This report provides a data-backed analysis of the global GSE market: current valuation, segmentation by power source and function, the growth forces reshaping the industry, regional dynamics, and the challenges operators face through the forecast period. Whether you're an airport operator, ground handler, or defense aviation professional, this is where the market stands — and where it's heading.

TLDR: Global GSE Market at a Glance

- The global GSE market was valued at approximately USD 6.14 billion in 2024, projected to reach USD 8.90 billion by 2034 at a CAGR of 3.8% (Polaris Market Research)

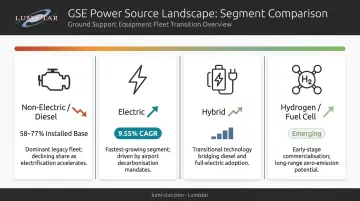

- Non-electric GSE holds the largest market share today; electric variants are the fastest-growing segment at 9.55% CAGR through 2031, outpacing all other power sources

- North America leads in market share; Asia-Pacific is expanding fastest, driven by new airport construction

- Air travel recovery, airport expansion, and zero-emission mandates are the primary growth drivers

- Key headwinds include high electrification costs, aging infrastructure, and labor shortages

Global GSE Market Size & Overview

Current Valuation and What the Numbers Actually Mean

The global GSE market sits at approximately USD 6.14–6.15 billion in 2024, with projections ranging from USD 7.45 billion by 2029 (MarketsandMarkets, 3.9% CAGR) to USD 8.90 billion by 2034 (Polaris Market Research, 3.8% CAGR). Some broader-scope estimates from IMARC Group place the 2025 market at USD 18.1 billion — a figure that reflects a wider scope definition, including categories the other reports exclude.

These variations reflect genuine differences in scope: some reports include only powered vehicles, others incorporate all equipment categories including non-powered tools, maintenance stands, and fixed infrastructure. The USD 6.1 billion figure from MarketsandMarkets and Polaris represents the most consistently defined commercial GSE baseline.

What's Driving Growth

The market's expansion ties directly to aviation's recovery and forward trajectory:

- Global passenger volume reached approximately 9.5 billion in 2024 — 104% of 2019 levels — and is forecast to exceed 12 billion by 2030

- IATA projects passenger traffic growth of 5.8% year-over-year in 2025

- ACI World estimates airports need USD 2.4 trillion in capital investment by 2040 to meet long-term demand

- Asia-Pacific and Middle East airports alone are projected to invest USD 240 billion from 2025–2035

Each new route, terminal, and aircraft in service creates corresponding GSE procurement demand. At scale, a single new long-haul route can require 15–20 additional GSE units to support daily operations.

Ownership Models and Equipment Categories

Two ownership dynamics shape market revenue. New equipment sales currently dominate — airports and airlines prefer modern, efficient fleets that meet emissions targets and reduce maintenance risk. The rental and lease segment is gaining ground, particularly among smaller operators and developing-market airports that can't justify large upfront capital commitments.

From a platform perspective, the market splits between:

- Conventional (commercial airport) GSE — the dominant volume segment covering all commercial airport operations

- Military GSE — smaller in volume but commanding premium pricing due to mission-critical requirements, weight ratings for military aircraft, and specialized functionality

The mobile vs. fixed equipment split also signals a meaningful shift. Mobile GSE (fuel trucks, belt loaders, tugs) holds the larger share due to operational flexibility. Fixed GSE — gate-integrated ground power units, pre-conditioned air systems — is growing as airports invest in permanent ramp infrastructure to cut emissions and congestion.

Market Segmentation Breakdown

Power Source: The Electrification Transition

| Power Source | Current Position | Growth Outlook |

|---|---|---|

| Non-electric (diesel/gas) | 58–77% of installed base | Declining share as mandates take effect |

| Electric | Fastest-growing segment | 9.55% CAGR through 2031 (Mordor Intelligence) |

| Hybrid | Included in market segmentation | Qualitative growth, no consensus share data |

| Fuel cell/hydrogen | Emerging, policy-eligible | Not yet a measurable share |

Several major airports have set near-term zero-emission ground operations targets that are creating forced replacement cycles:

- Amsterdam Schiphol targets emission-free ground operations across its Dutch airports by 2030, covering baggage tractors, pushback tractors, scissor lifts, and catering vehicles

- LAX mandates 100% zero-emission GSE by 2033, with conventional baggage tractors and belt loaders prohibited from January 2030

- Heathrow targets all airside vehicles zero-emission where possible by 2030 and has proposed £37 million for EV charging infrastructure

Functional Categories: Where Revenue Concentrates

Aircraft handling — tugs, pushback tractors, ground power units, deicing trucks — generates the most market revenue by a wide margin. Both IMARC Group and Mordor Intelligence place this category at roughly 53–54% of total GSE demand in 2025. Every aircraft movement requires pushback, power, and ground support regardless of route or aircraft type.

The five core functional categories are:

- Aircraft handling — tugs, pushback tractors, GPUs, deicing vehicles (largest segment)

- Cargo and baggage handling — belt loaders, container loaders, dollies (fastest-growing at 6.61% CAGR per Mordor)

- Passenger handling — jet bridges, stair trucks, apron buses

- Aircraft servicing — fuel trucks, lavatory service vehicles, water service carts

- Maintenance and safety — maintenance stands, jacks, towbars, rescue vehicles

Cargo and baggage handling's growth is driven by rising passenger volumes alongside e-commerce-fueled air freight demand at major hub airports.

Advanced and Smart GSE

Autonomous and connected equipment is moving from pilot programs to commercial deployment. Singapore's Changi Airport has deployed two fully driverless baggage tractors operating between Terminal 1 and Terminal 4, with plans to expand to 24 vehicles by 2027. TCR Group, operating GSE rental across 120 airports in 18 countries, partnered with Targa Telematics for real-time monitoring, maintenance support, and asset sharing across its fleet.

The smart GSE segment encompasses:

- IoT-connected telematics for real-time location and utilization tracking

- Predictive maintenance algorithms that reduce unplanned downtime

- AI-guided cargo loaders and autonomous baggage tugs

- Fleet management platforms with utilization analytics

Military and Defense GSE

Military GSE occupies a distinct category — mission-critical and purpose-built for high-stakes environments. This segment includes armament handling systems, aircraft tow vehicles rated for military aircraft weights, and specialized power supply units configured for defense platforms.

For defense flight test operations specifically, ground telemetry and data acquisition systems function as a distinct class of specialized GSE — supporting real-time data capture and transmission during test flights. Lumistar, based in San Marcos, California, manufactures modular ground telemetry systems including the LS-28-DRSM Series and LS-68-M Series for aeronautical flight test programs. Their systems comply with Range Commander's Council IRIG 106 requirements. They are deployed at federal test ranges across programs spanning supersonic aircraft development, UAV testing, and missile test operations.

Key Growth Drivers & Emerging Trends

Air Traffic Recovery and Fleet Expansion

The aircraft delivery pipeline is the clearest long-term demand signal for GSE procurement. Boeing forecasts demand for approximately 43,975 new commercial aircraft through 2043; Airbus projects roughly 43,400 deliveries over 2025–2044. Every new narrowbody or widebody entering service at a new airport requires a corresponding GSE fleet — tugs, GPUs, loaders, fuel trucks, and support vehicles — at both origin and destination.

Passenger traffic growth compounds this. The ACI/ICAO forecast of 12 billion passengers by 2030 translates directly into more aircraft turns per day, more baggage cycles, and more servicing events — each one requiring operational GSE.

Sustainability and Electrification

Regulatory pressure from IATA, ACI, and national aviation authorities is transforming electrification from an option into a timeline. Government grant programs are reducing the financial barrier: the FAA's Voluntary Airport Low Emissions (VALE) program funded Philadelphia International Airport's replacement of 228 pieces of GSE with zero-emission electric alternatives. The European Alternative Fuels Observatory links eGSE adoption to AFIR and Clean Vehicles Directive support, with AENA planning 890 airside charging points by 2030.

This drives a sustained upgrade cycle. Virtually every category of powered GSE — from baggage tugs to deicing vehicles — now has an electric or hybrid alternative entering commercial availability.

Automation and Digital Integration

Airports are deploying IoT telematics and predictive maintenance platforms to reduce GSE downtime and cut operating costs. The same push toward networked ground systems is reshaping defense flight test infrastructure, where ground stations must integrate with digital range networks for real-time data access.

Lumistar's LS-28-DRSM Series reflects this shift in the flight test segment. The system converts RF telemetry data to UDP TMoIP packets over Ethernet, enabling distributed real-time access by engineering teams. During Virgin Orbit's LauncherOne mission, it captured telemetry throughout the entire flight for both live monitoring and post-mission analysis, with PTP (IEEE-1588) time synchronization ensuring data integrity across the range network.

Emerging Market Airport Investment

The scale of airport construction in Asia-Pacific and the Middle East is creating unprecedented GSE procurement demand from scratch:

- India plans to develop 50 additional airports within five years, targeting up to 350 airports by 2047

- China targeted more than 270 civil transport airports by end-2025

- Vietnam's Long Thanh International Airport Phase 1 opened in December 2025, representing a USD 4.6 billion Phase 1 investment in a multi-phase USD 18.7 billion project

- Dubai's Al Maktoum International Airport Phase 2 carries an AED 128 billion investment, targeting 150 million passengers annually

- Saudi Arabia's King Salman International Airport targets 100 million passengers by 2030

Each of these projects enters service with zero existing GSE inventory, meaning full-fleet procurement across every functional category from opening day.

Regional Market Landscape

North America: Largest Market, Sustained Leadership

North America holds between 34% and 54% of global GSE market share — a wide range that reflects differences in scope definition across research firms, with higher figures typically including military and defense GSE alongside commercial aviation. Its leadership rests on several durable factors:

- Extensive network of high-frequency international airports with consistent equipment replacement cycles

- Early adoption of electric GSE driven by state-level emissions regulations (California, in particular)

- FAA grant programs that de-risk electrification investment for airport operators

- Substantial military aviation activity — U.S. Air Force bases and federal test ranges maintain significant GSE fleets, including specialized defense and flight test ground equipment

Asia-Pacific: Fastest Growing

Asia-Pacific leads all regions in growth rate. Mordor Intelligence projects a 6.94% CAGR through 2031, driven by expanding middle-class air travel demand, budget airline proliferation, and government-mandated airport expansion across India, China, Vietnam, and Indonesia. The USD 240 billion Asia-Pacific and Middle East airport investment figure from ACI represents direct GSE procurement demand at scale.

Europe, Middle East, and Beyond

The remaining regions each reflect distinct demand drivers:

- Europe: Growth is sustainability-led. EU climate mandates are accelerating electric GSE adoption, with Schiphol and Heathrow serving as operational benchmarks for zero-emission ramp operations

- Middle East: Dubai and Saudi Arabia are positioning as global aviation MRO hubs, with GSE demand fueled by new airport builds on an unprecedented scale

- Latin America and Africa: Smaller markets with longer investment horizons — ACI estimates Latin America needs USD 94 billion in airport infrastructure through 2040, translating to significant GSE procurement demand as projects come online

Challenges & Future Outlook

Three Structural Headwinds

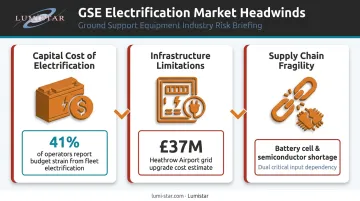

1. Capital cost of electrification The 2024 Ground Support Worldwide industry survey found that 41% of respondents cited equipment costs as their heaviest budget strain. Electric GSE isn't just a vehicle purchase — it requires charging infrastructure, grid capacity upgrades, and operational scheduling changes that smaller airports and handlers in developing markets often can't absorb.

2. Infrastructure limitations Legacy airports face physical and electrical grid constraints that slow eGSE deployment. Heathrow's £37 million charging infrastructure proposal illustrates the scale of investment required even at a well-resourced hub.

3. Supply chain fragility Component shortages — batteries, semiconductors, high-grade metals — are extending lead times and raising prices across electric and hybrid GSE categories. These disruptions hit the most advanced equipment categories hardest, the same categories where demand is growing fastest.

Workforce and Skills Gap

The same survey found 43% of respondents citing training on new technologies as a major difficulty, with finding and retaining skilled staff ranking as the top operational challenge for a second consecutive year. Operating and maintaining smart GSE — autonomous tugs, telematics-integrated fleets, electric ground power systems — requires competencies that the current aviation ground workforce often lacks.

The same gap shows up in specialized defense environments. Military flight test ranges depend on operators who can work fluently across the hardware and the data streams it produces — a combination that's hard to hire for and harder to develop quickly. Lumistar addresses this through structured training programs and unlimited post-delivery technical support, covering everything from PCM format analysis and ground station fundamentals to site surveys and system configuration.

Forward Outlook

Through 2030 and beyond, the market trajectory points toward:

- Widespread electrification at major hubs, driven by mandates at LAX, Schiphol, and Heathrow creating demand that cascades to second-tier airports

- Deeper AI and IoT integration for predictive fleet management, reducing downtime and improving utilization across large equipment fleets

- Expanded public-private partnerships financing sustainability upgrades at airports that can't self-fund the transition

- Continued greenfield procurement demand from Asia-Pacific and Middle East airport builds

For defense aviation and flight test professionals, the infrastructure stakes are rising alongside program complexity. Test programs for supersonic aircraft, advanced UAVs, and next-generation military platforms are generating more data than ever — and the ground systems that capture, process, and distribute that telemetry in real time have to keep pace.

Frequently Asked Questions

How big is the ground support equipment market?

The global GSE market was valued at approximately USD 6.14 billion in 2024 and is projected to reach USD 8.90 billion by 2034 at a CAGR of 3.8% (Polaris Market Research). MarketsandMarkets projects a similar baseline reaching USD 7.45 billion by 2029. Higher estimates, such as IMARC Group's USD 18.1 billion for 2025, reflect a broader methodological scope and are not directly comparable.

What are the two types of ground support equipment?

GSE is broadly classified into non-powered equipment — chocks, dollies, maintenance stands, service stairs — which require no independent power source, and powered equipment — ground power units, tugs, fuel trucks, belt loaders, deicing vehicles — which have their own power source for operational functions. Most market revenue analysis focuses on the powered category.

What are the 5 major categories of ground handling services?

The five categories are:

- Aircraft handling and movement

- Cargo and baggage handling

- Passenger services and boarding

- Aircraft servicing (fueling, lavatory, water, catering)

- Maintenance and safety operations

Each relies on specialized GSE, with aircraft handling generating the largest share of market revenue.

What is driving growth in the global GSE market?

Four factors are driving GSE market growth:

- Post-pandemic air travel recovery, with global passenger volumes projected near 12 billion by 2030

- Large-scale airport construction across Asia-Pacific and the Middle East

- Fleet modernization cycles at established hubs

- Regulatory mandates requiring airports to replace diesel GSE with electric alternatives

Which region dominates the ground support equipment market?

North America currently holds the largest market share, supported by its extensive airport network, high flight frequency, early electric GSE adoption, and significant military aviation activity. Asia-Pacific is the fastest-growing region, driven by rapid airport expansion and rising passenger demand across India, China, Vietnam, and surrounding markets.